The results of some interesting experiments to report here from the work of my colleague Carlos Garriga and his coauthors, Roman Sustek and Finn Kydland. DA

The statement from the July

meeting of the Federal Open Market Committee reveals a support for starting to

increase interest rates this Fall, provided some further improvement in the

labor market. Such monetary policy stance is currently held also by policy

makers in the U.K., as hinted by some members of the Monetary Policy Committee,

the rate-setting body of the Bank of England.

An important channel through

which interest rates affect the typical household is the cost of servicing

mortgage debt. Standard mortgage loans require homeowners to make nominal

installments—regular interest and amortization payments—calculated so that the

loan is fully repaid by the end of its term. Changes in the interest rate set

by the central bank affect the size of these payments, but differently for

different types of mortgage loans. In addition, the real value of these

payments depends on inflation.

Mortgage contracts and debt

servicing costs

Fixed-rate mortgages (FRM),

characteristic for the U.S., have a fixed nominal interest rate and thus

constant nominal installments for the entire term of the loan, typically 15 or

30 years. The FRM interest rate is determined at origination on the basis of

the mortgage lenders’ expectations of the future path of the central bank

interest rate. In contrast, the interest rate of adjustable-rate mortgages

(ARM), a standard contract in the U.K., changes every time the central bank

interest rate changes. The nominal installments of ARM loans are thus

recalculated on every such occasion, to ensure the full repayment of the loan

by the end of its term.[2]

While mortgage contracts

specify nominal installments, either fixed of adjustable, the real cost of

servicing mortgage debt depends on inflation. The effects of the liftoff on

homeowners will therefore depend not only on the mortgage type and the future

path of interest rates but also on what happens to inflation during the

liftoff.

It is instructive to illustrate the effects of the liftoff

on homeowners in terms of changes in mortgage debt servicing costs

(DSC)—nominal mortgage payments deflated by inflation as a fraction of

household real income. This variable provides a metric of the burden of

mortgage debt to homeowners as it measures the fraction of real income

homeowners have to give up to meet the mortgage payment obligations of their

contract. The numerical examples below illustrate these points.[3]

Liftoff scenarios

Figure 1 considers two alternative paths of the central

bank interest rate, a slow liftoff and a fast liftoff from the current nearly

zero lower bound (ZLB). In both cases, the interest rate is assumed to revert

to 4 percent, the pre-2007 crisis average. In the fast liftoff case, it reaches

the half-way mark of 2 percent in two years’ time, whereas in the slow liftoff

case this mark is not reached until about eight years from the start of the

liftoff.

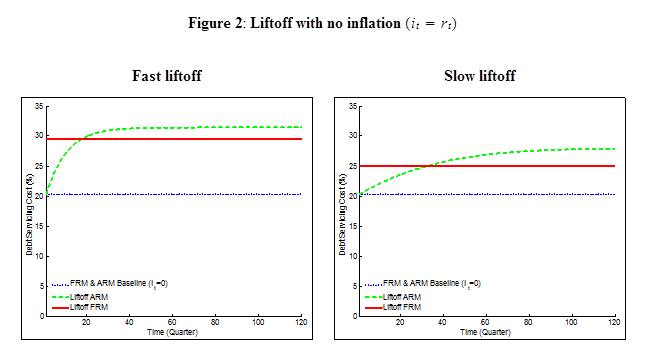

Figure 2 plots DSC in the case of liftoff that is not

accompanied by an increase in inflation. In this case the path of the nominal

interest rate in Figure 1 coincides with the path of the real interest rate.

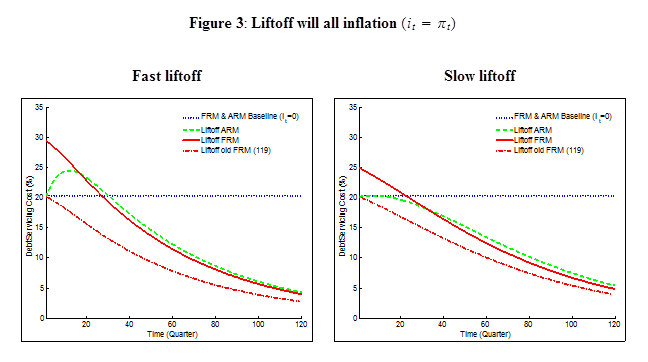

Figure 3 contrasts this case with a situation where the increase in the central

bank interest rate is accompanied by a one-for-one increase in the inflation

rate. In this case, the real rate is left unchanged at zero percent and the

path of the nominal interest rate in Figure 1 is equivalent to a path of the

inflation rate. While both assumptions are extreme, they demonstrate how the

effects of the liftoff depend on the inflation rate.

In both figures, the DSC under the various liftoff

scenarios are compared with a baseline case, in which both the central bank

interest rate and the inflation rate stay unchanged at zero percent (blue

dotted line), approximately the current situation. In this case, DSC are about

20 percent due to the assumed lenders’ markup of three percentage points.

A liftoff without inflation

When inflation stays at zero percent during the liftoff

(Figure 2) the real mortgage payments of existing homeowners with FRM loans are

unaffected. This is because the FRM interest rate has been fixed at origination

before the liftoff and inflation stays at zero percent. However, new FRM loans

will be priced according to the expected path of the central bank interest rate

in Figure 1 and will therefore carry a higher interest rate. The new FRM

interest rate is higher the faster is the liftoff. In the case of the fast

liftoff, the higher interest rate implies DSC of almost 30 percent; under the

slow liftoff, DSC will be 25 percent (the solid red lines in Figure 2).

When mortgages are ARM, the liftoff affects both, existing

and new homeowners. The dashed green lines plot DSC for new ARM homeowners and

essentially track the paths of the central bank interest rate—DSC gradually

increase from 20 percent to 32 percent under the fast liftoff and to 27.5

percent under the slow liftoff. For existing homeowners with ARM the effects

depend on when the loan was originated. The more recently originated was the

loan the more will the path of DSC resemble that for new loans. DSC of loans

that are almost repaid will be almost immune to the liftoff. This is not only

because the debt outstanding gets smaller over the life of the loan, but also

because mortgage payments in later periods of the life of the loan are mostly

amortization payments, rather than interest payments.

A liftoff accompanied by inflation

When the liftoff is accompanied by equivalent increase in

inflation, and no change in the real rate, the impact of the liftoff on DSC is

greatly attenuated (Figure 3). First, existing FRM homeowners gain from the

higher inflation and these gains grow over time as persistent inflation

deflates the real value of the nominal payments, which under FRM are constant.

Those with the more recently originated mortgages gain the most over their

homeownership tenure (the dash-dotted red lines in the figure show the case of

a mortgage with 119 quarters remaining; that is 29 years and 3 quarters). New

FRM borrowers, however, will face a higher mortgage rate and, as a result,

initial DSC of almost 30 percent in the fast liftoff case (solid red line). But

the real value of those payments will also gradually decline over

time.

For ARM homeowners, both the existing and new homeowners,

there are two opposing forces in place. On one hand, higher nominal interest

rates increase nominal mortgage payments. On the other hand, higher inflation

reduces their real value. The first effect is stronger initially but the second

effect dominates over time. Furthermore, the point where the second effect

starts to bite depends on the speed of the liftoff. While in the fast liftoff

case the first effect dominates for the first eight years (32 quarters), in the

slow liftoff case it hardly bites at all (dashed green lines).

Policy implications

To sum up, the effects of the liftoff on homeowners depend

on three factors: (i) the prevalent mortgage type in an economy (FRM vs ARM),

(ii) the speed of the liftoff, and (iii) what happens to inflation during the

course of the liftoff.

If inflation stays constant at near zero then in the U.S.,

where FRM loans dominate, the liftoff will affect only new homeowners. In the

U.K., where ARM loans dominate, the negative effects will in contrast be felt

strongly by both new and existing homeowners.

However, if the liftoff is accompanied by sufficiently

high inflation as in our examples, the negative effects will be much weaker in

both countries. In the U.S., the initial negative effect on new homeowners will

be compensated by positive effects on existing homeowners. And in the U.K.,

provided the liftoff is sufficiently gradual, neither existing nor new

homeowners may face significantly higher real costs of servicing their mortgage

debt.

Therefore, if the purpose of the liftoff is to “normalize”

nominal interest rates without derailing the recovery, central bankers in both

countries should wait until the economies convincingly show signs of inflation

taking off. Furthermore, the liftoff should be gradual and in line with

inflation.

Buzz words: “If the purpose of the liftoff is to

“normalize” nominal interest rates without derailing the recovery, the Federal

Reserve Bank and the Bank of England should wait until the economies show

convincingly signs of inflation taking off.”

Carlos

Garriga

Research Officer

Federal

Reserve Bank of St. Louis

(314)

444-7412

carlos.garriga@stls.frb.org

[2] In the U.K., the

typical mortgage is the so-called standard-variable rate mortgage, which has an

interest rate fixed for the first year or two. After this initial period, the

interest rate can vary at the discretion of the lender, but usually the resets

coincide with changes in the Bank Rate, the Bank of England policy interest

rate. A “tracker” mortgage is explicitly linked to the Bank Rate. Here we

abstract from these details.

I would argue that in the forgoing context wage inflation (perhaps using the ECI as a proxy) is a more insightful deflator of mortgage interest costs, and hence the impact of various liftoff scenarios, than a general price-level deflator like CPI. What do you think?

ReplyDeleteI am embarrassed to say that I did not know that 15- and 30-year fixed rate mortgages were so common in the USA.

ReplyDeleteInteresting, particularly in light of the activist stance of the US central bank.